Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

FinTech is considered one of the most highly regulated industries and the fastest-moving at the same time. All products from digital payment systems and lending platforms to wealth management applications and neobanking apps adhere to strict compliance standards like KYC, AML, PCI-DSS, and financial regulations specific to different regions.

However, even with all its importance, the compliance process often remains overlooked by many teams working on their FinTech projects. As a result, it slows down the project launch considerably, poses security threats, and imposes restrictions on architecture.

Operating fintech is considered one of the most regulated environments. This helps shape an evolved global financial regulation in fintech. Further, this could play a significant role in influencing everything from payments to digital banking.

A leading fintech application development company knows for sure that compliance is not only a legal obligation but a critical aspect of design. By introducing compliance early in the development process, a company can increase the speed of growth and success in the market.

Compliance is an incredibly strategic element in a way most teams do not anticipate. Compliance affects not just penalties but also the overall reliability and scalability of the product, as well as its user trustworthiness.

The main benefits of compliance in Fintech include:

For the companies involved in custom fintech app development, this approach will help avoid any further issues, additional expenses for rework, and technical debt. Compliance done correctly becomes an instrument for business growth.

As per the industry research at PWC about the impact of trust and security in fintech adoption, 1compliance-driven systems are likely to gain long-term customer confidence.

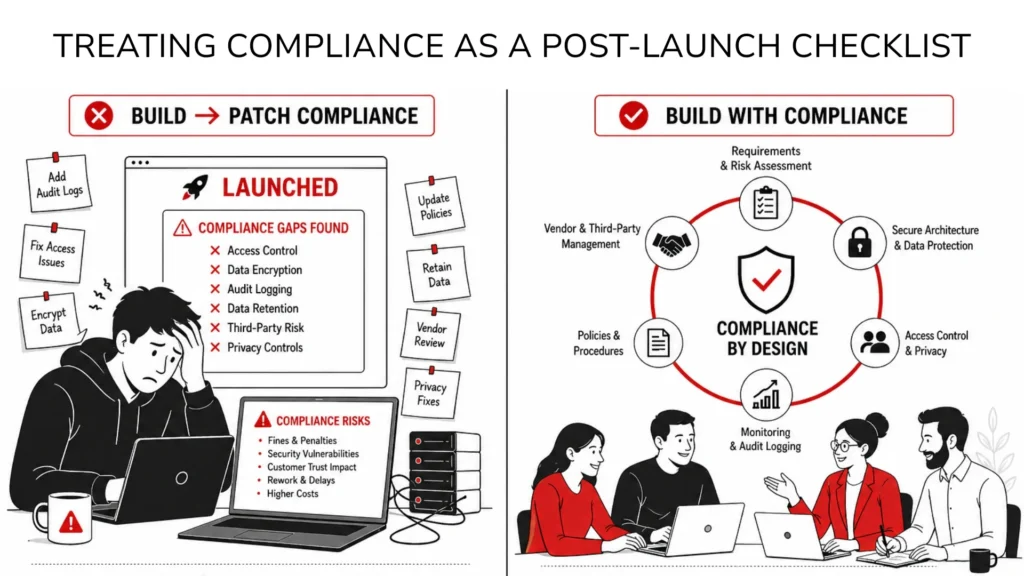

Many teams will construct their product first and then try to “build in compliance after the fact.” Compliance becomes a checkmark to be validated right before the product goes live.

Compliance requirements are an integral part of architecture, database design, encryption strategy, identity management, logging, and API integration. None of these can be easily added on after the fact.

Those teams that postpone compliance usually find themselves redesigning core systems. Modern systems should integrate compliance in the early stage, further aligning with secure software development lifecycle guidelines, which can be placed in security into every development phase.

Compliance is usually managed by lawyers and risk managers who operate independently from the engineers and product managers.

Compliance requires technical knowledge. It entails:

Lack of coordination results in the development of functionalities that do not adhere to compliance standards.

According to the experts, the importance of collaboration in compliance and engineering teams ensures security controls are implemented at architecture level.

Financial technology apps depend a lot on third-party solutions such as payment gateways, KYC verification solutions, fraud protection tools, etc. Often, teams believe that the vendors themselves are entirely compliant.

Even if vendors are compliant, your app is accountable for:

In summary, when you hire fintech app developers, it is important to ensure they know about vendor risks.

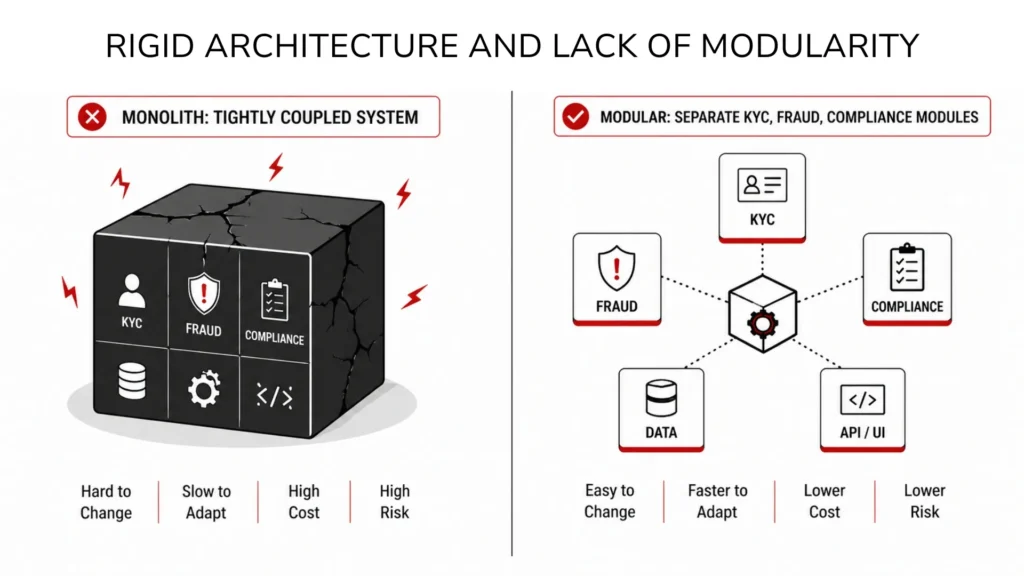

FinTech software solutions are designed to be monolithic systems that have compliance logic embedded into the application itself.

Compliance regulations keep changing, making it hard for any monolithic system to cope with such changes, such as:

Systems need an open architecture to cope with the challenges mentioned above.

Cross-platform mobile app development services with modular backend systems help avoid such problems.

Teams concentrate more on developing features without considering data encryption, logging, and auditing.

FinTech applications need to:

It is mandatory, not a choice, to have an audit trail.

Data security is a necessity for FinTech applications.

The flow of consents by users tends to be unclear, misleading, or complicated. User consents are regarded by teams merely as a formality.

Various regulations, including GDPR, necessitate:

Both regulatory compliance and usability are necessary for the consents.

Using AI chatbot app development services helps optimize the consent flow by making it conversational and intuitive for users.

Rather than viewing compliance as the last step, build it into each phase of the development process:

The compliance-first approach can be suitable for reflecting security by design principles in application development, where risks are mitigated before development.

In this way, compliance will become an integral part of the system rather than a layer added to it. Firms providing Custom Mobile App Development Services in the United States are incorporating compliance by design concepts into their applications to comply with strict financial regulations right from the start.

Modular design enables compliance functionality to be separated from application functionality. This makes it possible to:

For instance:

This is essential in the constantly evolving landscape of regulatory compliance.

Manually compiling compliance reports is tedious and error-prone. Modern FinTech software must:

Automation helps eliminate human errors and keeps the system prepared for audits at any moment. Companies using Custom Mobile App Development Services in the United Kingdom are increasingly relying on automated compliance pipelines for more efficient and cost-effective regulatory reporting.

Data integrity is central to FinTech compliance. Software teams should ensure that all data is:

Each piece of information must be:

Although ensuring compliance requires strong data integrity and access control best practices, which also includes RBAC logs.

Compliance in FinTech is more than just trying not to get fined – compliance means creating something your customers can use and which regulators will approve of.

And what is the most common mistake a team could make when developing a FinTech product? The same thing as always – thinking about compliance as an afterthought. On the contrary, compliance will define your architecture, workflows, and UX/UI since day one.

Why? Because taking a compliance-first approach helps:

As FinTech keeps moving forward to 2026 and even further, the winning products will not be those with the most functionalities. They will be safe, secure, and flexible.

These are the challenges:

Among all the threats, compromised cybersecurity and unauthorised access can be harmful. These can lead to fraud, identity theft, and data theft.

Some of the success factors in fintech are funding, networks, responsiveness, organizational governance, entrepreneurial culture, internal communication, compliance centricity, etc.

These are the metrics considered in the fintech business: customer acquisition cost, lifetime value, monthly recurring revenue, retention rate, and net promoter score.